China may release a softer trade data this week, short AUD/USD?

Data shows slacks remain in US labour market despite drop in unemployment rate

US unemployment rate has fallen below 4% for first time since Bill Clinton era. However, we do not expect Fed to alter its monetary policy for this new development.

The jobless rate dropped to 3.9 % in April, its lowest since the end of 2000 while nonfarm payroll grew by 164,000 during this month. Wage growth was disappointing, at 2.6% over the year, well below pre-financial crisis rates that exceeded 3%. Regardless, US is adding jobs at a healthy pace even though the country is eight years into the post-crisis expansion with monthly payroll gains averaging 200,000 so far this year. This is underpinning the Fed’s willingness to carry on lifting short-term rates and next move is widely expected in June. Nevertheless, there remains signs of further slack in parts of the labour market, including the mixed news on wage growth, suggesting there is no extra need for the Fed to accelerate the pace of rate rises.

Bank of England likely to signal “delaying rate hike, not ceasing”

In late March, a May hike from the Bank of England seemed like a done deal, but a run of disappointing data has since conspired to rub out that expectation. BOE will want to convey the message that holding steady in May doesn’t signal a policy shift. We expect the next hike to be in August instead. The MPC’s policy decision and minutes of its May meeting and new economic forecasts will be released on 10 May. Beyond the near term, we doubt there will be any significant changes to the path of growth which is the key reason why we don’t expect BOE to alter its policy outlook. That should mean that 2019 and 2020 GDP growth forecasts are unchanged. With the yield curve in a similar position to February, the weakness at the start of the forecast horizon is likely sufficient to prevent the economy from overheating towards the end of the projection period.

Watch the inflation signal closely as it may give you a better Fed’s rates path outlook

Following Powell’s speech, the major theme of the week will be inflation data with producer prices release on Wednesday, consumer prices on Thursday and consumer sentiment/inflation expectations on Friday. The PPI will be watched for evidence of tariff-related price pressures working through supply chains.

Our Picks

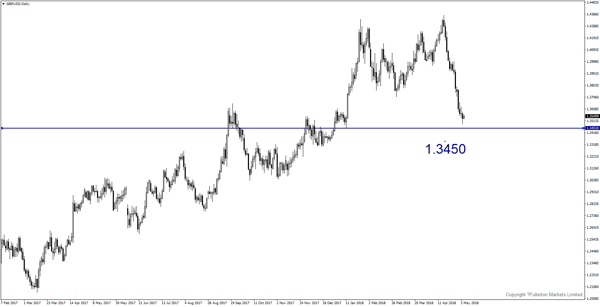

GBP/USD – Slightly bearish.

BOE may hold the rate this week, and this pair may drop towards 1.3450.

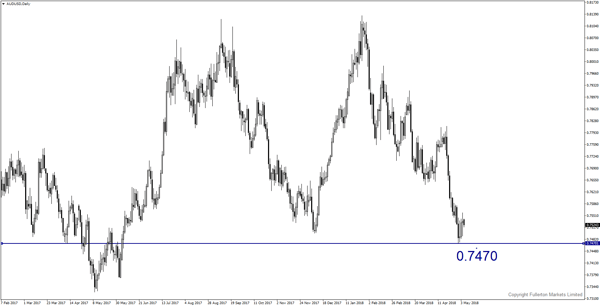

AUD/USD – Slightly bearish.

China may release another soft trade data this week, AUD/USD may drop towards 0.7470.

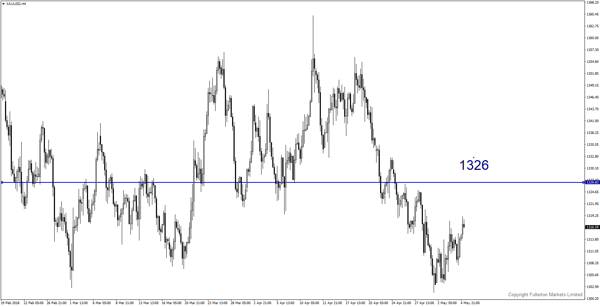

XAU/USD (Gold) – Slightly bullish.

We expect price to rise towards 1326 this week.

Fullerton Markets Research Team

Your Committed Trading Partner