Market will start to evaluate the progress of the economy reopening, which may offer some bids to risk assets, long USD/JPY this week?

The big rotation into cyclical stocks, like banks, small caps and airlines, took a break Friday, but it could be a theme that dominates trading again in the week ahead, as investors will be assessing the progress of economic reopening against some new headwinds for the market. In addition to the jobs report, there is important ISM manufacturing data Monday and auto sales for the month of May.

The stock market has been mostly discounting unprecedented weakness in economic data, but the May employment report will still be of major interest this Friday. Market expects it to show another shocking loss of jobs, this time roughly 8.5 million after the 20.5 million loss in April. The unemployment rate is expected to jump to a staggering 19.8% from 14.7% in April.

The increasingly frayed relations between the US and China reared up at the end of the week as a negative force for markets, and traders expect that stress to continue to be a concern. Market will continue the tug of war as investors dip into value names versus some of the growth names in tech, and the stocks that had benefited from the stay-at-home trade.

We saw this early as the market came off the March lows, market tried to say what do we need now, what do we need when this is over. Meanwhile, healthcare and pharma started to get a very strong bid. On the other hand, social media and tech firms face dual headwinds, and that could hold back the overall market as well since they had been leaders in the move off of the March lows. Trump on Thursday issued an executive order aimed at limiting legal protections of social media companies, after he got into a disagreement with Twitter. Hence, there’s a ratcheting up of pressure on technology and social media firms, with a lot of overlap in big tech in terms of China’s exposure.

Big tech stocks have lagged lately, but they are still a top leader quarter to date, with a 20% gain. In the past week, they were up about a half percent, compared to a 6% gain in financials and 5% rise in industrials. As tech lagged, so did the Nasdaq, gaining only a third as much as the Dow in the past week.

On average, the market is weaker in the medium term when you had that kind of massive outperformance. The message is that both the finance and technology tend to be weaker in the medium term. In the long term, you go back to the idea that the rotation into financials is a positive. S&P 500 may be hitting the top of a near-term range, after it broke through the 3,000 level, a key psychological point. It also broke through its 200-day moving average, a widely watched technical level. Some investors see a buy signal when the S&P is above that momentum indicator, which is literally based on the average closing level of the index over the last 200 days.

The stocks that have outperformed recently are the most sensitive to the economic reopening leading to a pickup in normal activity. There is a question of how much air traffic or hotel stays can pick up until there is real medical progress against the virus. These stocks will be a matter of intense debate for months. We don’t think we’ll know the answer until we see if the fall brings a ratcheting higher of the virus, based on reopening and a change in the weather, or if there’s a change in progress on a vaccine.

Our Picks

EUR/USD – Slightly bullish.

This pair may rise towards 1.1140 this week

USD/JPY – Slightly bullish.

This pair may rise towards 108.20

XAU/USD (Gold) – Slightly bearish.

We expect price to drop towards 1710 this week

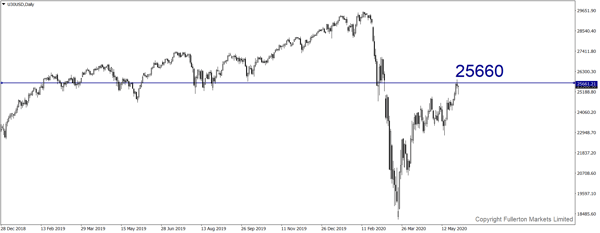

U30USD (Dow) – Slightly bullish

Index may drop towards 25660 this week

Fullerton Markets Research Team

Your Committed Trading Partner