As the odds of a rate cut increases after a worse-than-expected US job report, investors may start to price in one more rate cut this year. Short USD/JPY?

While factory hiring posted a modest contraction, goods sector employment continued to rise. Similarly, service industry subcategories continue to be vulnerable to factory conditions. Manufacturing may be witnessing a short-term soft patch, but tangentially related industries, in both a literal and figurative sense, have "kept on trucking.”

Nonfarm payrolls rose 136k in September, below the forecast of an earlier consensus at 135k. This thereby confirms that as GDP growth slowed below 2% in the second half, the pace of hiring will diminish as well. The decline in the unemployment rate to 3.5% exceeded expectations for a one-tenth drop. This shows that even a slower pace of hiring will be sufficient to tighten labour conditions.

Government hiring masked a significant deceleration in the private sector. The former added 22k jobs, mainly in the state and local government (census-related hiring was negligible at 1k), while private companies created 114k jobs in September. On a six-month moving average basis, government hiring accelerated to 22k from close to zero in the beginning of the year, while private job creation slowed to 133k from 227k in January.

Even so, labour-cost pressures remain quiescent. The muted factory recession impact, evident in the latest jobs data, is testament to the resilience of economic growth at present. Our subjective estimate of recession risk through year-end 2020 remains around 20%, even though model-based measures, particularly those utilising yield curve signals, tend to show a higher probability.

Average hourly earnings growth slipped to the lowest in more than a year, presenting some risk to consumers, who currently hold up the economy’s growth. Overall, the trend for job gains is stepping down. The three-month moving average for private payrolls sits at the lowest since 2012, as employers add fewer workers. Manufacturing jobs contracted by 2,000 during the month, the second time that has happened this year. It came amid the recession in the industry in the US.

A core element of the recession estimate was based upon the expected resilience of consumer spending over this period. So long as job growth remains sufficient to prevent a destabilisation of the unemployment rate (roughly 100k per month based on our estimates), consumer prospects will then be at least strong enough to prevent a growth stall. Even as the unemployment rate touches 3.5%, a level last seen in 1969, wage pressures remain tame. This should give policy makers the confidence to maintain, or even augment, monetary accommodation as insurance against downside risks.

Our Picks

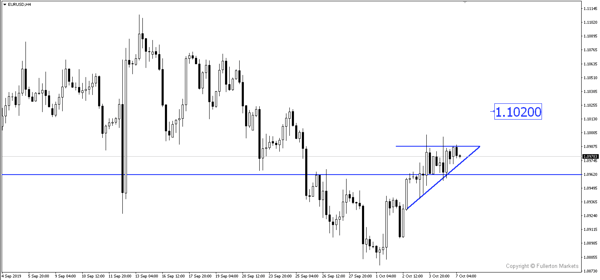

EUR/USD – Slightly bullish.

This pair can rise towards 1.0200 if US CPI continues to miss forecast this week.

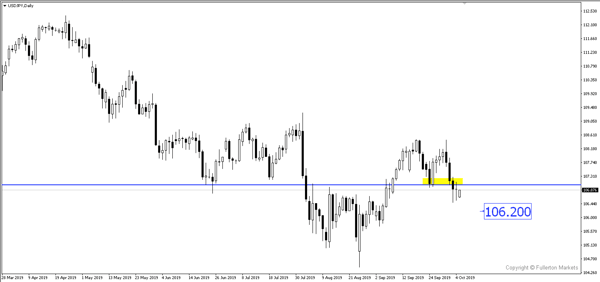

USD/JPY – Slightly bearish.

As long as 107.30 is not broken, this pair may continue to head lower towards 106.20 due to increase in odds of a rate cut.

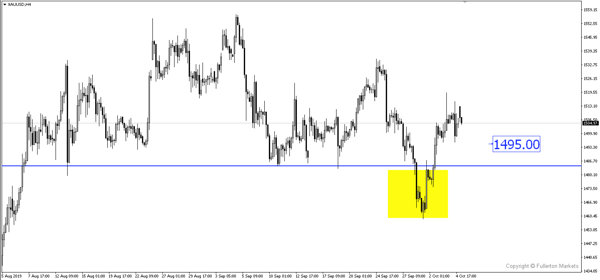

XAU/USD (Gold) – Slightly bearish.

We expect price to fall towards 1495 as US-China trade sentiment improves.

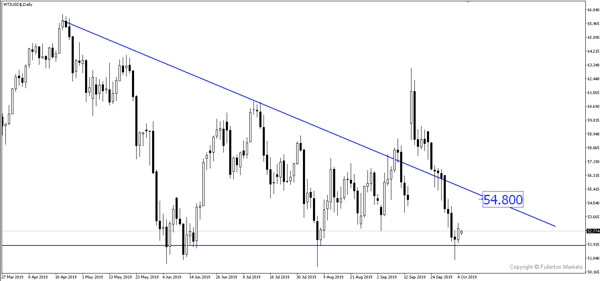

Crude oil (WTI/USD) – Slightly bullish.

Crude oil may rise towards 54.80 after rebounding off a strong support as seen from the chart.

Fullerton Markets Research Team

Your Committed Trading Partner