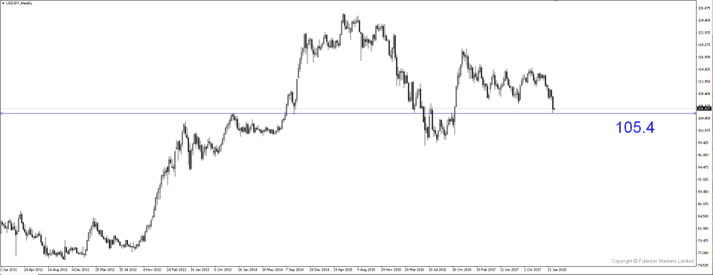

Inflation worries, and concerns will continue to pressure the dollar, continue selling USD/JPY?

Dollar continued to slide last week as we see a fresh 3 year low in the overnight session,

with yen falling below at 106 to the greenback for the first time since November 2016.

Although the US massive amount of fiscal injection is nothing new, the current low unemployment rate accompanied by strong activity growth makes the situation unusual.

The big question is why is US dollar weakening? Higher bond yields and US rates rising should have, in theory, boosted the dollar. In the FX market, the conventional correlations are partly linked to the shift in capital flows. This explains the rise in foreign demand for assets in Eurozone and Japan due to a huge current account surplus. The weak dollar is also the reason why Wall street and global share markets rebounded so quickly as their foreign revenues are boosted by a weaker home currency.

US CPI rose more than expected in January by 0.5% versus a forecasted 0.3%, marking the fifth consecutive month of CPI growth that is at or above Fed’s target of 2%. Currencies normally would rise as higher inflation means a stronger probability of a rate hike which will lead to inflow to the currency to capture those higher rates. However, this isn’t the case as the dollar gains fizzled out. The reason is that the market is not so worried about inflation per se, but instead Fed is now forced to play catch up and at the same time shrinking their balance sheet which worries investors.

Thursday’s FOMC meeting minutes should be a good indicator on its view over the outlook for inflation. As a rate hike in March is almost certain at this point, the FOMC minutes will reinforce those expectations of an upgraded inflation outlook. Furthermore, the US tax deal and possible higher stimulus from the government that causes stronger inflationary pressure might be the key topic given that the Fed is looking to tighten this year.

Traders have to monitor US yields carefully as it might pose a serious danger to the markets and the economy. The 10-year Treasury Note passed the 2.9% level on 15 February. If they peak at 2.9%, we should see a stronger recovery in USD/JPY. However, if 10-year rates head towards the 7-year high at 3.04%, the bears will return.

The prospect of widening twin deficits is giving the bears more reason to remain bearish. Twin deficit, on its own, does not tell us a lot about the direction of the dollar. During the Reagan era, the dollar rose to all time high as deficits climbed. While during the George W Bush era, the dollar rally in the early period before falling as trade balance collapsed. How the dollar moves as the prospect of widening twin deficits will be very much based on FOMC reaction. If they feel that the current fiscal stance is a threat to its inflation target, there could be further tightening which could lead to a stronger dollar.

Our Picks

USD/JPY – Slightly bearish.

Thursday’s FOMC meeting should set the direction for how the dollar will move for weeks to come.

We are expecting a cautious stance which will lead to deeper losses.

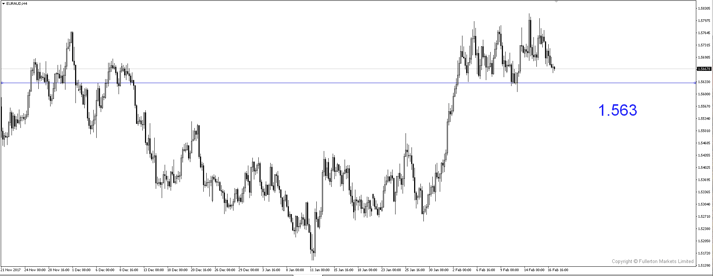

EUR/AUD – Slightly bearish.

Technically, we are expecting this pair to retest its major support at 1.563 as RBA Governor Lowe mentioned that they are not worried about the level of the currency.

This is followed by a recovery in commodities like iron ore and copper.

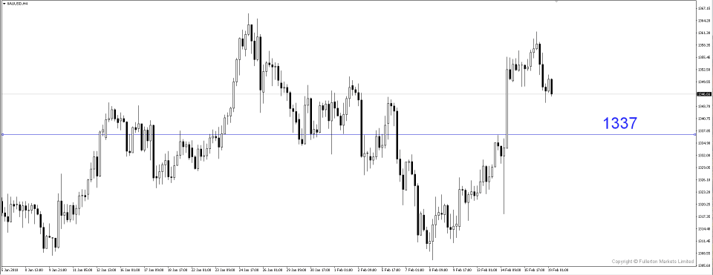

XAU/USD (Gold) – Slightly bearish.

Gold rallied from 1318 to 1360 following the CPI report last week. 1360 level proved to be a strong resistance.

Friday’s sell-off and reversal points to further downside to the support at 1337

Fullerton Markets Research Team

Your Committed Trading Partner